Why the U.S. Thrives in Global Competitiveness

Related Articles

As characteristics of the U.S industries, we can list mature IT industry and financial systems, labor market flexibility, strong growth of startups, and high technological development and innovation capabilities. Recently, the U.S. is becoming increasingly competitive in the areas of state of cluster development and multi-stakeholder collaboration, as well as willingness to delegate authority and companies embracing disruptive ideas, and the U.S. is among the contenders for the top ranking in global competitiveness.

Also, compared to Japan and other countries, the U.S. has increasing competitiveness in workplace and education-related skills, such as skillset of staff and graduates and ease of finding skilled employees. For digital competitiveness, the U.S. ranks world number one. The possible reasons behind this include progress in big-data analysis and application and venture capital availability, in addition to the introduction of robots and development of digital legislations.

The U.S. advantage comes not only from technological development capacity for promoting manufacturing but also from producing GAFAM (Google, Amazon, Facebook, Apple, and Microsoft) that made use of existing information and communication technologies and logistics to promote social transformation. These companies introduced significantly advanced goods and services—product innovation—and improvement of process in sales and delivery methods—process innovation. Although there still are concerns about post-COVID economy and employment recovery, the U.S. is expected to continue to expand its industrial competitiveness.

Ⅰ. Innovation Breakthroughs and Rising Labor Productivity

Innovation is essential to enhance industry competitiveness, expand wages and employment, and long-term economic growth in the U.S. When we look at examples of major technological advances in the U.S. over the past 180 years, they include Alexander Graham Bell’s telephone in 1876, electromagnetic motors which relates to transportation machineries in 1888, the Wright Brothers’ airplane in 1906, Du Pont’s nylon fiber in 1938 and vinyl in 1940, the Internet by the Defense Advanced Research Projects Agency (DARPA) in the 1960s, recombinant DNA technology by Stanley Cohen and Herbert Boyer in 1980 and 1984, and the 1-Click ordering system in 1999.

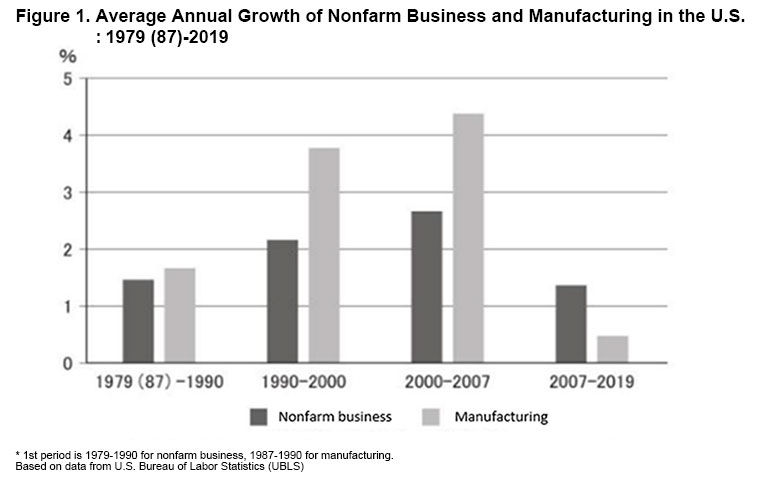

Progress in technological development and innovations in the U.S. can become the factor for boosting productivity. As shown in Figure 1, the average annual growth rate of labor productivity (value added productivity per hour) in U.S. nonfarm business and manufacturing sectors continued to increase from the 1980s to 2007. However, with the spread of the financial crises that began in 2007, the average annual growth rate of U.S. labor productivity slowed down during 2007-2019 in both nonfarm business and manufacturing sectors. This is one reason the average growth rate of the U.S. GDP declined since the financial crisis.

Even in the 2010s, U.S. labor productivity still suffered from the aftereffects of the financial crisis. This may also be due to overseas transfer of manufacturing facilities from globalization. Basically, domestic production and employment are shifting to China, Mexico, and other countries.

In Figure 1, during 2007-2019, the manufacturing sector shows a lower average annual growth rate than the nonfarm business sector, suggesting relatively higher growth in the service sector.

Since the 1990s, the U.S. has been transferring domestic production sites overseas while shifting domestic industries to a service economy. In the so-called deindustrialization, the U.S. has been leading the world. We all know this led to the subsequent rise of the information, knowledge, and service industries and the birth of GAFAM.

Meanwhile, Figure 2 shows the average annual growth rate of labor productivity in the major service sectors in the U.S. from 1987 to 2018. Among them, software publishers, cable and other subscription programming, wired and wireless telecommunications carriers, travel arrangement and reservation services, commercial banking, and accounting and bookkeeping services were the sectors that increased labor productivity during this period.

As expected, from the 1980s to the present, the U.S. labor productivity growth rate has been consistently high in the services sector such as leisure, finance, and technical expertise, as well as IT-related areas that include GAFAM. It is apparent these sectors have continued to boost the U.S. global competitiveness.

Ⅱ. Biden Administration’s Policies for Boosting Competitiveness

When Joe Biden becomes the U.S. President, he will be oriented towards a big government resulting from higher taxes and increased expenditure for infrastructure investment, and is likely to promote the Buy American plan and develop policies focusing on domestic employment.

Biden has stated that he will invest a record 2 trillion USD over the next four years as part of environmental measures and seek to rejoin the Paris Agreement. With this, including expenditures for additional economic measures and health care, and increased social security costs, some estimate about 10 trillion USD increase in spending over 10 years. As for trade and foreign policy, while adopting multilateral discussions, no change is expected in the tough stance toward China.

On July 9, 2020, in a speech in the swing state of Pennsylvania, Biden announced his economic revitalization plan. He vowed to “Build Back Better” the U.S. and made clear his stance to support the American middle class through the Buy American rule. Biden’s political issues are the following five points: (1) strengthen the domestic industrial base, (2) create an economy with long-term strength, (3) strengthen support for working parents, (4) strengthen support for the working class and small businesses, and (5) comprehensive measures for racial equity.

Biden has proposed to implement federal procurement of U.S. products and raw materials worth 400 billion USD over the four years of his first presidential term for the development of storage batteries and next-generation materials and energy equipment to modernize infrastructure. A working group on environmental measures will be established in the White House, and a new division of environmental and climate justice will be created within the Department of Justice. He will raise the corporate tax rate, which was lowered to 21% by the Trump administration, to 28%, and intends to collect federal income taxes from Amazon.

Also, to counter China’s unfair trade practices, Biden seeks to “Innovate in America” by making 300 billion USD investment over four years in research and development (R&D) and breakthrough technologies such as battery technology, artificial intelligence (AI), biotechnology, and clean energy. For example, in addition to technologies for electric vehicles (EVs) and lightweight materials, he plans to invest in high-value manufacturing and technology such as 5G and AI to unleash high-quality job creation. These measures by Biden to promote science and technology seem reminiscent of the innovation strategies of the Obama administration.

Biden has announced building 500,000 charging stations to promote EVs, as well as providing incentives to encourage consumers to replace gas cars with EVs. Automakers and suppliers will be given incentives to invest in production facilities, while 3 million government fleet will also be replaced with EVs.

Some of these measures by Biden to support innovation overlap with President Trump’s protectionist economic and trade measures, in that they aim to expand production and employment in the domestic industries. Yet, unlike President Trump’s implementation of additional tariffs and sanctions through bilateral talks, this approach seems different in terms of ensuring quality employment while raising the competitiveness of domestic industries.

Ⅲ. Why the U.S. Boosted Its Competitiveness

The World Economic Forum (WEF), headquartered in Geneva, Switzerland, releases the Global Competitiveness Report. According to the WEF, the U.S. ranked second in global competitiveness in 2019 on the backdrop of outstanding strength in areas such as business dynamism, innovation capability, and financial system, as shown in Table 1. Although a rank lower than the previous year, it is still a notch higher from third place in 2016.

The U.S. is globally competitive, helped by the growth in the service sector productivity as well as the high level of manufacturing sector’s productivity (value-added amount). The strong competitiveness of the U.S. service sector can be perceived from the fact that it was where the GAFAM was born, while all five companies rank among the world’s top ten in market capitalization.

According to the data from the Boston Consulting Group, the average annual growth rate of U.S. manufacturing productivity (value of output per worker) increased by only 1.1% over the five-year period from 2013 to 2018, while Japan, Germany, and China expanded by 3.3%, 2.4%, and 7.3%, respectively, over the same period. However, for 2018 alone, the U.S.’s growth rate from the previous year increased by 4%, higher than 3% for Japan or 2% for Germany.

Besides, the 2018 value of output per worker in the U.S. was 111,000 USD, higher than 81,000 USD in Japan, 90,000 USD in Germany, or 28,000 in China. This means, during 2013-2018, the U.S. had a lower average growth rate in manufacturing productivity than Japan, China, or Germany, but maintained a higher absolute value of output per worker.

Backed by the above factors, U.S. global competitiveness is rising. The first reason is that the U.S. outperforms the world in innovation capability.

The U.S. has the solid environment and conditions for promoting technical revolutions, such as well-functioning multi-stakeholder collaboration, research institutions prominence, and a high number of citations for papers. As a country with an influx of immigrants, the U.S. has systems for transferring professionals from overseas, and people actively move within the domestic labor market. The relevant laws and legal systems that trigger innovation are in place, and there is widespread freedom and deregulations necessary to promote smooth business activities.

The second reason for the strong U.S. global competitiveness is the business dynamism embedded within the U.S. industries. That is, in U.S. industries, there is a market mechanism that allows ideas to be realized and principle of competition to function, along with the use of ICT and digitization and progress in technological development. Furthermore, there is an environment for people to move or start a business easily, as well as the business dynamism that enables shifts to industry structures that has high-value and potential.

The third reason is that new startups are popping up in succession with generous financial support. This probably comes from the flexibility in the U.S. business system, which responds adequately and promptly to the changes in the environment and circumstances of the times. For example, as can be seen in the cases of GAFAM, U.S. companies have succeeded in being among the first to develop and introduce businesses using a platform or other forms and create and popularize high-value industrial sectors as a pioneer in the world.

Also, the U.S. has created many startups by utilizing incubators which are common in California’s Silicon Valley. The manager of an incubator supports the creation of a new business by cleverly matching startups with venture capitalists who provide the funds. The managers become well versed in cross-industry businesses through experience in various positions by frequent job changes.

To develop such talent, it is essential that the U.S. labor market functions flexibly and the environment for nurturing competent managers experienced in technology and corporate management works effectively. Thus, the strong competitiveness for human resource development and financial support system in the U.S. also seems to contribute to the creation of startups.

Fourth, promptly moving plants overseas and promoting manufacturing outsourcing must have also enhanced the U.S. global competitiveness. Apple’s smartphones and Dell’s computers are typical products enjoying the benefits of globalization.

Fifth, to protect domestic industries, the U.S. has implemented hard-line trade policies and supported American companies to increase export and expand overseas, or restricted investments within the U.S., which in part may have led to the recovery and revitalization of the U.S. industry. Examples from the past include the Japan-U.S. trade talks on semiconductors, steel, and cars.

More recently, the Trump administration placed export control on China’s Huawei and others by revising the Export Administration Regulations, and restrictions on foreign investment in the U.S. by the Committee on Foreign Investment in the United States (CFIUS), to expand U.S. domestic production and employment and reduce trade deficits, or control Chinese and other foreign investment in the U.S. from the perspective of national security.

Ⅳ. Areas Where the U.S. Enjoys High Competitiveness

Among the pillars of U.S. globalization competitiveness listed in Table 1, the areas in which the U.S. ranks highly in 2019 are business dynamism (1st), innovation capability (2nd), financial system (3rd), labor market (4th), and skills (9th).

Similarly, in 2019, Japan ranks 17th for business dynamism, 7th for innovation capability, 12th for financial system, 16th for labor market, and 28th for skills. So in the areas important for global competitiveness, the U.S. has a significant advantage over Japan. Moreover, the U.S. has raised its ranking from 2016 to 2019 in both innovation capability and business dynamism, while Japan was up a notch in innovation capability but moved down in business dynamism.

Table 1 shows the U.S. global competitiveness using the 12 pillars as the index. For Table 2, I have selected 23 components in which the U.S. has high competitiveness rankings in 2019. There are about 100 components distributed across the 12 pillars as more detailed indicators.

Table 2 shows that among the 23 components of global competitiveness, the U.S. ranked first in the following eight: legal framework’s adaptability to digital business models, ease of finding skilled employees, redundancy costs, internal labor mobility, venture capital availability, insolvency regulatory framework, scientific publications, and research institution prominence.

The U.S. ranked second in the following seven components: financing of SMEs, gross domestic product, attitudes towards entrepreneurial risk, growth of innovative companies, companies embracing disruptive ideas, state of cluster development, and multi-stakeholder collaboration.

They are third for domestic credit to the private sector, fourth for buyer sophistication, fifth for E-Participation, skillset of graduates, and hiring and firing practices, sixth for extent of staff training, and seventh for willingness to delegate authority and diversity of workforce.

Among these components, the U.S. has moved up its rankings annually in venture capital availability, state of cluster development, and extent of staff training.

In old school thinking, we would have listed financial system efficiency, labor market flexibility, growth of venture companies, and technological developments and innovation capability as the reasons for the strong industrial competitiveness of the U.S.

However, what emerges from Table 2 is that the workplace and education-related components, such as extent of staff training (component 6.02 in Table 2, ranked 6th), skillset of graduates (6.04, 5th), and ease of finding skilled employees (6.06, 1st) are supporting the pillar Skills (6th pillar in Table 1, 9th).

Also, as factors for rising U.S. competitiveness in Business Dynamism (11th pillar in Table 1, 1st), in addition to insolvency regulatory framework (component 11.04 in Table 2, 1st) and attitudes towards entrepreneurial risk (11.05, 2nd), it is surprising to find components like willingness to delegate authority (11.06, 7th) and companies embracing disruptive ideas (11.08, 2nd).

Similarly, as factors for the rise in Innovation Capability (pillar 12 in Table 1, ranked 2nd), state of cluster development (12.02, 2nd), multi-stakeholder collaboration (12.04, 2nd), and buyer sophistication (12.09, 4th) are included together with scientific publications (12.05, 1st).

In contrast, although Japan has the top position for 2019 patent applications (per million population, U.S. ranking: 13th), it ranks only 27th in willingness to delegate authority in Table 2. It is thought-provoking that Japan has continued to decline each year in state of cluster development (12th) and multi-stakeholder collaboration (25th) that had been considered the source of its industry competitiveness.

Meanwhile, for the components in Table 2 in which the U.S. outperforms, Japan is no match for the U.S., ranking 106th for diversity of workforce, 75th for internal labor mobility, 58th for attitudes towards entrepreneurial risk, 48th for companies embracing disruptive ideas, 42nd for skillset of graduates, and 30th for growth of innovative companies. This means Japan falls far behind the U.S. in not only employment system and venture development but also in the competitiveness of corporate vitality such as industry clusters and multi-stakeholder collaboration, and the environment for generating innovation.

Yet, although still behind the U.S., Japan is highly competitive for scientific publications (6th) and research institutions prominence (7th). Japan is also ranked high for patent applications (per million population, 1st) and R&D expenditures (% GDP, 6th). Therefore, by leveraging on these intellectual assets, Japan should aim to further enhance its overall global competitiveness.

Ⅴ. Overwhelming U.S. Strength in Digital Competitiveness

1. The U.S. Leads for Three Consecutive Years

Located in Switzerland, like the WEF, the International Institute for Management Development (IMD) has been releasing the IMD World Digital Competitiveness Ranking since 2017.

According to the fourth Digital Competitiveness Ranking released in 2020, the U.S. continued to rank the highest among 63 countries. In 2020, Singapore was 2nd, Denmark was 3rd, Sweden was 4th, and Hong Kong was 5th. Japan ranked 27th, declining from 23rd in 2019. South Korea was 8th (10th in 2019), so all these countries outperformed Japan.

In the 2017 results, the U.S. ranked 3rd, behind Singapore and Sweden. The U.S. rose to the top spot in 2018 and 2019, followed by Singapore and Sweden. Basically, these three countries have been the top three contenders since 2017, and the U.S. has managed to stay on top for three straight years from 2018 to 2020.

2. U.S. Ranks High in Scientific Concentration and Adaptive Attitudes

As shown in Table 3, IMD analyzes and evaluates each country’s digital competitiveness using the three factors of “Knowledge,” “Technology,” and “Future Readiness.” Each of the three factors is divided into three sub-factors, and each sub-factor is further divided into criteria as shown in Table 4. The 63 countries are ranked for each criteria.

For example, in 2020, the U.S. ranked 1st in the “Knowledge” factor, which is broken down into sub-factors of “Talent (14th),” “Training and Education (24th),” and “Scientific Concentration (1st),” as shown in Table 3. The sub-factor “Scientific Concentration” comprise criteria such as “R&D productivity by publication (3rd),” “Robots in Education and R&D (3rd),” “High-tech patent grants (5th),” and “Total expenditure on R&D (% of GDP) (10th),” as shown in Table 4.

As shown in Table 3, the U.S. topped the global digital competitiveness ranking in 2020 by being 1st in “Knowledge,” 7th in “Technology,” and 2nd in “Future Readiness” factors. Moreover, its 1st place in “Scientific Concentration,” the sub-factor of “Knowledge,” and 2nd place in both “Adaptive Attitudes” and “Business Agility,” the sub-factors of “Technology,” must be the backdrop for its increased competitiveness.

As the underlined criteria in Table 4 shows, we can point out that the U.S. is highly competitive in “Scientific Concentration” helped by both “R&D productivity by publication” and “Robots in Education and R&D” criteria ranking in 3rd place. Under the “Capital” sub-factor, “Venture capital (1st),” “Banking and financial services (2nd),” and “Funding for technological development (2nd)” criterion rank high.

Similarly, under “Adaptive Attitudes,” the U.S. is highly competitive in the criterion of “Tablet possession (1st),” “E-Participation (1st),” and “Internet retailing (2nd),” while under “Business Agility,” the criterion “World robots distribution (4th),” “Use of big data and analytics (9th),” and “Knowledge transfer (9th)” are strong.

The U.S. has good academia-business collaboration, with smooth knowledge transfer and use of venture capital. It has many scientific publications, and scientific research legislation for igniting innovation is in place. There is efficient support by banks and other financial institutions, and application and analysis of big data, providing the environment for developing a digital economy.

3. U.S. Digital Competitiveness Remains Strong Post-COVID

The U.S. has been enjoying the top position in IMD’s digital competitiveness ranking, and it is likely to become more competitive in the post-COVID future. Amid the worsening impact of the pandemic, the moves by Google. Amazon, Facebook, and other GAFAM companies are under attention.

Amazon is expected to add over 100,000 new jobs in North America even after the pandemic, while Google and Facebook are expected to increase their customer services. Apple, too, has recovered its smartphone production in China and its new products and devices essential for working from home appear to be selling well.

As the pandemic continues to have a negative impact on the U.S. economy, the darlings of information and communications like GAFAM are expected to see further growth in new business models and e-commerce utilizing the internet in the post-COVID world. In other words, triggered by the pandemic, GAFAM will further expand and contribute to the recovery of the U.S. economy.

In addition, as indicated by IMD, the U.S. has high capacities for “venture support,” ” banking and financial services,” and “internet retailing competitiveness,” and the environment is in place for the further development of the digital economy after the pandemic. In addition, other factors contributing to boost U.S. digital competitiveness include the high R&D productivity by publication and robots in education and R&D, not to mention internet utilization. Therefore, the prior investments in the digital economy are well used, and the U.S. is expected to maintain and expand its high digital competitiveness, with GAFAM playing the main role.

When President Biden takes office, he is likely to promote U.S. innovation and invest heavily in emerging technologies and R&D of new industries such as EVs, battery technology, AI, 5G, and clean energy, and the creation of high quality jobs. We will see whether the Biden administration can smoothly shift its economic policy toward clean energy and other “strategic promotion of industrial competitiveness,” in the face of the protectionism and anti-globalization trend promoted by President Trump.

Reference:

“Will the COVID Ignite Innovation?” Institute for International Trade and Investment (ITI), column no. 78, May 29, 2020 (in Japanese)

“Prevent Japanification by Digitizing” Institute for International Trade and Investment (ITI), column no. 79, June 18, 2020 (in Japanese)

“Increasingly Strong U.S. Business Dynamism and Innovation Capability: Japan-U.S. Comparison of Global & Digital Competitiveness” International Trade and Investment Quarterly No. 121, September 2020 (in Japanese)

Toshiki Takahashi

Chief Researcher, Institute for International Trade and Investment (ITI). Joined Japan External Trade Organization (JETRO) in 1976, and worked in JETRO New York Center. After being Director of International Economic Research Division and Director-General of Overseas Research Department, takes on the current position from 2011. Taught as a part-time lecturer at Chuo University and Toyo University. Author of many books, including “Canada’s Economic Growth and Japan” (in Japanese, from Akashi Shoten, 2005), “Asia FTA Strategies for Japanese Companies” (in Japanese, from Bunshindo, 2016).

JA

JA EN

EN